A Deep (But Not TOO Deep) Explanation of Anti-Money Laundering Regulations

As a gallery owner or dealer, you should be familiar with Anti-Money Laundering regulations and have certain practices in place to protect your business. Learn more by reading our user-friendly guide.

As a gallery owner or dealer, you should be familiar with Anti-Money Laundering regulations and have certain practices in place to protect your business. If you don’t already, or you’d like to know more to be sure you’re doing the right things, read our user-friendly guide. We’ve simplified the legal jargon so you don’t need to be a legal expert to understand what steps to take for your business.

What Is Money Laundering?

Money laundering is the process that criminal organizations engage in to make their illegally gained money seem legal or ‘clean’ by depositing through legitimate businesses.

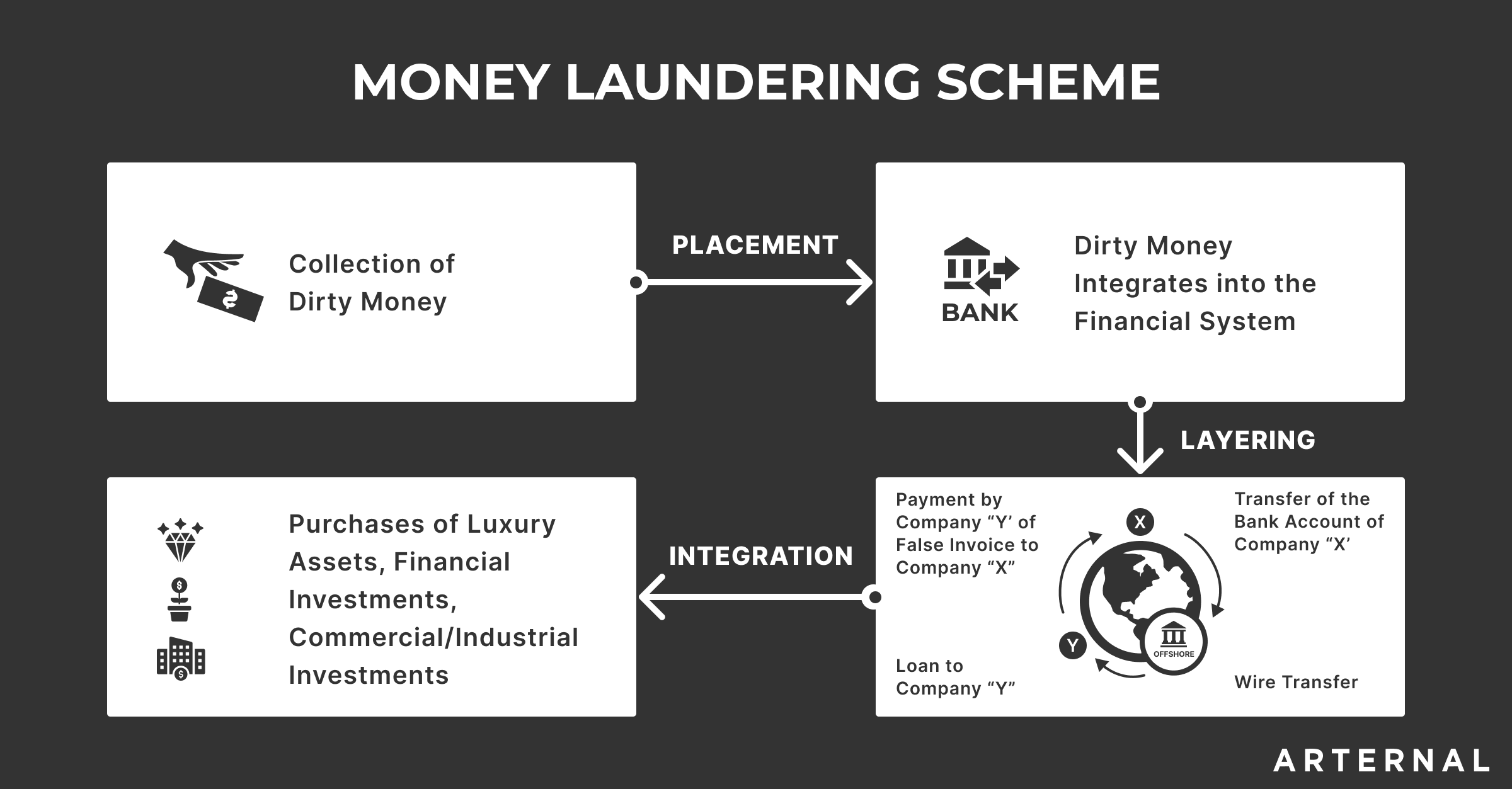

Money laundering typically involves three steps: placement, layering, and integration.

Placement: Involves depositing ‘dirty’ money into a ‘clean’ legitimate business.

Layering: Disguises the original source of the money, through multiple transactions and usually bookkeeping fraud.

Integration: The money is then withdrawn from the legitimate business(s) and reintroduced into the legitimate economy (Investopedia).

Why Art is an Ideal Vehicle for Laundering Money?

Art is an appealing method for laundering money for a number of reasons. The main ones that appeal to criminals are that it can be smuggled, transactions can be private, and prices are subjective, can be manipulated, and extremely high as a luxury good (The National Law Review). There is also often inconsistent or poor record-keeping keeping when it comes to art sales.

Why is Money Laundering Getting Worse in the Art Market?

Along with the reasons above, criminals have been more active in the art market, making money laundering more of a risk for businesses and individuals that sell art.

With the rise of international terrorism and organized crime, most countries have adopted consistent regulations to identify fraud and suspicious activity for financial services and gambling, leaving a hole for criminals to engage more in the art market (Keystone Law).

In addition, the rise of technology, encrypted communication, and the challenges of international enforcement have all played a role.

What Are The Compliance Requirements?

As a gallery, dealer, auction house, or other business involved in art sales, it’s possible for you to unknowingly engage with individuals involved in purchasing art for money laundering purposes. Therefore it’s important to understand the following standards for AML.

The Responsible Art Market Standard and the Basel Institute Standard are the best to reference for businesses operating in the US. They have a lot of common guidelines outlined in the next section below.

Note regulations do vary by country so if you’re based outside the US then it’s best to reference the Responsible Art Market Standards Guide for your specific country of business. Use the list below as a general guide, but first and foremost make sure that you’re familiar with local laws and are operating under the requirements within your country of business.

Stay up to date on the latest from ARTERNAL

What Are The Practical Steps You Need to Take for AML Compliance?

Both the RAMS and BIS noted above recommend the following steps to ensure your business is AML compliant:

1. Do a Risk Assessment of Your Business

Experts advise adopting a “risk-based” approach for your business. To determine the level of risk your business is exposed to, consider the following questions:

- What security measures do you already have in place?

- What types of transactions do you engage in? What types of payment do you accept?

- What information about your clients do you record?

- What research is done on your inventory?

- What controls are in place to check the source and legitimacy of funds?

- What training is provided to staff?

- Are procedures reviewed regularly? Is there room for improvement?

2. Know Your Clients and Establish Their Risk Profiles

The most important step of being AML compliant is to establish a good understanding of your clients, creating a risk profile, and understand how to spot red flags. Here are some steps you should take:

- Verify identification, understand if you’re doing business with an individual or a legal entity like a company, foundation, or trust.

- Understand if you’re doing business with a third party purchasing for another individual if this is the case, understand who the Beneficial Owner is (the ultimate receiver of the artwork).

- Client screening – set up a process to screen your clients, so you have an understanding of where they reside, do business and the source of their wealth and art collection

- Keep an eye out for red flags

- PEPs – politically exposed persons

- The client is known to be or associated with someone involved in a criminal or regulatory investigation, and/or conviction

- The client lives, operates, or banks in higher-risk jurisdictions

- Offshore companies, trusts, foundations, or institutions

- Agents for anonymous buyers or sellers

3. Know the Artwork Provenance

If you’re working in the primary art market and the artwork has never previously been sold, all you need is to know the artist and verify they are the creator of the work.

If you’re working in the secondary art market, there is a higher risk of art fraud, so it’s important that you have a clear history of ownership and provenance documented.

- Keep an eye out for red flags

- Limited or no documentation

- Seller is reluctant to provide documentation

- Antiquities where the source country is in recent conflict

- Keep an eye out for red flags

4. Know the Background and Purpose of the Transaction

In addition to knowing your customer, make sure you know what the purchase will be used for. You should also evaluate the form of the transaction and the method of payment.

When considering the form of the transaction ask – is it face to face, solely online, between intermediaries? If it’s not facing to face, you may need to seek further information from the client to verify the legitimacy of the transaction.

When considering the payment method ask – is it cash, done through a third party, a bank account located in non-AML regulated jurisdictions? All these factors could indicate a red flag. Other transaction red flags to consider:

- Client is reluctant to provide information regarding their identity

- Client provides identification that is invalid

- Client insists on paying with an anonymous credit card or cash card

- Client operates through multiple private investment companies or offshore structures

- Client insists on paying a large amount in cash

- Client insists on paying separate low-value transactions for a single transaction

5. Keep Records

While having up-to-date and accurate bookkeeping is important for your business to function, adopting record-keeping around your risk assessment measures is an important step for several reasons. It allows you to make an informed decision about whether to continue with a transaction or not. It allows you to monitor and evaluate your processes in place. You can keep an eye out for customer trends. In the case criminal activity occurs, it allows you to respond and comply with any legal obligations from law enforcement.

6. Create a Standard Operating Procedure, Train Staff, and Monitor Processes

Create steps and a procedure for your staff to identify risk and red flags and make sure there are actionable steps for them to verify the validity of a client. Include training on what to do if the client cannot be verified or they suspect the client is engaged in unlawful activity.

Be sure to monitor and review your SOP and training and make any adjustments to the process as needed.

7. Know How to Act and Report

As a business owner, you have the right not to do business with anyone you suspect is fraudulent. If you have well-founded suspicions that a client is engaging in money laundering or terrorist financing you should refrain from doing business with them. The next step would be to report the suspicions to the authorities in the case where reporting is mandatory (again this will vary by local laws, certain countries have mandatory reporting requirements).

When you’re making an assessment based on the red flags outlined above, note that they are used to paint a picture of a potentially fraudulent transaction. A single red flag doesn’t always mean the client is illegitimate, that is when you may need to follow up for more information and insight. Usually, there are multiple red flags that comprise a more complete picture, so use your best judgment accordingly and err on the side of caution.

Technology Can Help Identify and Prevent Risk

Financial tools and analytics can help recognize red flags, identify patterns, and in turn help you prevent potential fraudulent activity.

One example is a tool from Deloitte, Art 360. The program “is designed to help identify and triage to what extent a potential art transaction or holding exposes an entity to fraud, non-payment, legal jeopardy, and other risks” (Deloitte).

Blockchain is another tool that can potentially help mitigate risk. It is the technology that serves as a public ledger for all bitcoin transactions made internationally and many believe can be used to create transparency and security around art sales (Artsy).

ArtAML is a new platform that helps individuals and businesses selling art perform all AML checks and is compliant with AML standards.

Conclusion

Whether or not you feel your business is at high risk for money laundering crime, the unfortunate truth is that it is a problem for the art market. If you’re in the business of selling art it’s important that you understand the risks and make sure you’re taking the necessary steps to comply.

You might also like these articles:

Interested in taking your gallery to the next level? Contact us today to learn more.